Everything you need to know about the Uni Pay 1/3rd card

Uni Cards that grew $18.5 million in the budget has newly come up with their Uni Pay 1/3rd card as their first offering to enhance user knowledge in the credit card industry. Here's everything you ought to know about the Uni Pay 1/3rd card.

Uni Cards that grew $18.5 million in the budget has newly come up with their Uni Pay 1/3rd card as their first offering to enhance user knowledge in the credit card industry. Here's everything you ought to know about the Uni Pay 1/3rd card.

What's Uni Pay 1/3rd Card?

Uni Pay 1/3rd card is technically NOT a credit card precise though it works primarily to a regular credit card on the cover. It's a PayLater card (or) Pay 1/3rd card, telling you, you can spend 30,000 INR this month and pay 10,000 INR a month for the next three months without any interest/fee.

The tech coating is absorbing as it uses:

- RBL/SBM bank's Prepaid card design on the surface that gives entrance to Visa

- NBFC partner (LiquiLoans) that delivers access to the credit line.

So ideally speaking, it's a household prepaid card. You cannot use it for global transactions or cash withdrawals and may also have issues loading wallets, as RBI rules control that from happening, which is anticipated to be cleared in a few months.

Fees & Charges

| Joining Fee | Nil |

| Renewal/Annual Fee | Nil |

| Interest on revolving amount | Late fees only, as per the slab |

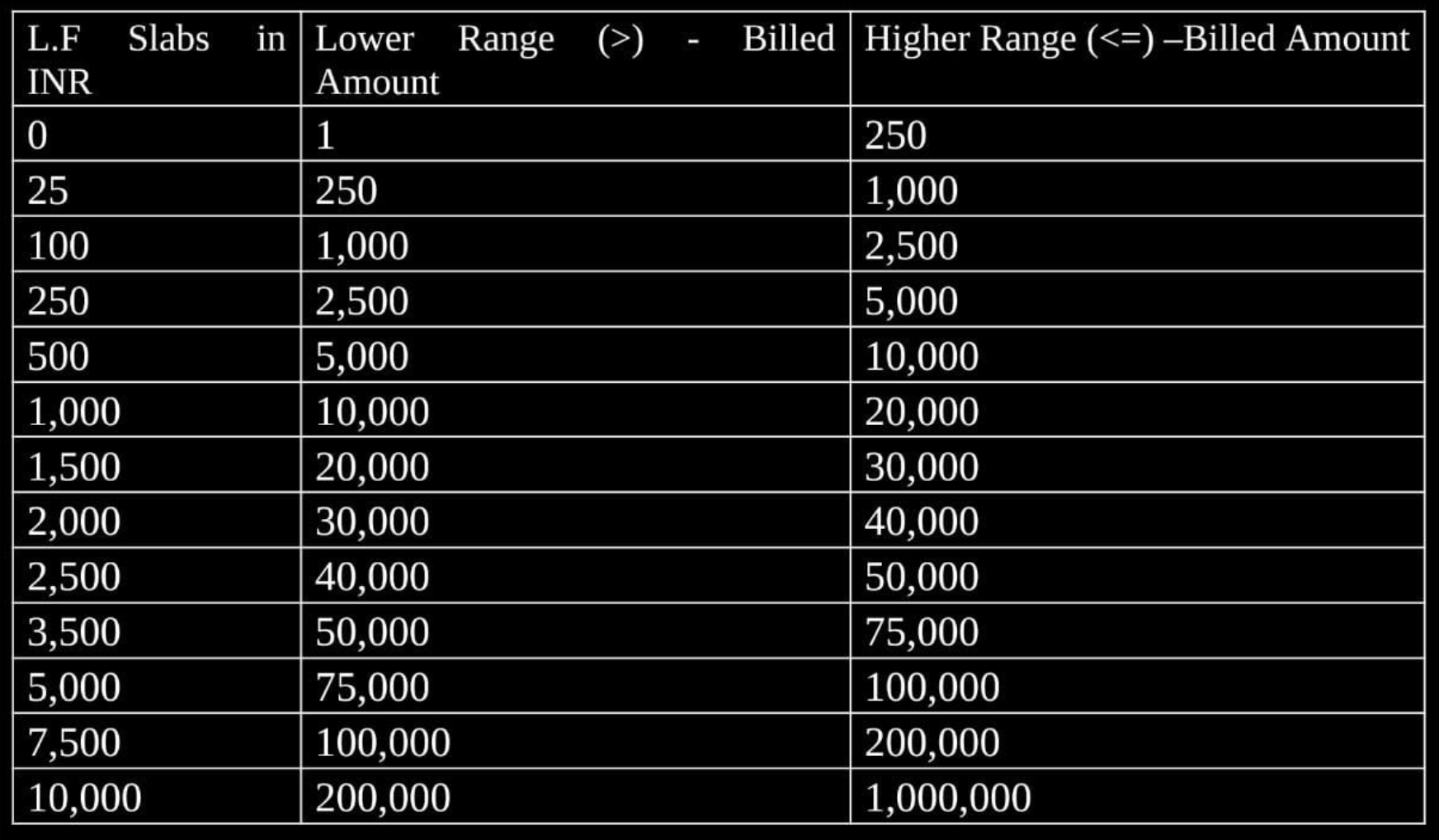

It’s ideally a Lifetime Free card (for now) and comes with a decent late fee slab system (instead of daily interest).

Rewards

- 1% Cashback to Card (if paid in full)

The method splits "each payment" into three parts by default, but you can decide to pay in full and enjoy 1% cashback.

The cashback system is super easy as you can select the transaction you like to pay in full in a few taps, and it immediately adjusts the cashback to unbilled stmt, just like below.

It's a good understanding; however, 1% is a bit lower even for entry-level cards as we've cards that give 2% cashback these days.

That said, Unicards does say that they're operating on a rewards system that lets you earn Uni Coins along with a Uni Store that gives 5X rewards (maybe like HDFC smart buy).

Design

Uni Card arrives with a neat and clean design with a title on the front and card points at the back, just like most other current premium cards issued these days. The card comes in a soft grey/silver color that looks decent.

Credit Limit

One of the multiple critical elements of an entry-level card is the credit limit. Most card issuers give a reasonably low limit, mainly when the first card with the bank.

Uni, however, states that they can issue cards with credit limits ranging from 20,000 INR to 6 Lakhs which sounds promising.

That's good for an entry-level card, and my credit limit was somewhere in the mid.

Credit Limit Enhancement requests can be sent after six months of card issuance.

Unboxing

The card arrives in a neat and well-designed box with a great premium feel. Initial impressions were like unboxing an iPhone instead of a card, great work on that!

The box comes with:

- The Uni Card

- A Toblerone chocolate (Yeah!)

- A Mask (good quality)

- A personalized baggage tag (looks beautiful)

Support

Yet another vital aspect when it arrives in entry-level cards is consumer support, which is almost non-existent in the industry because of the volume.

Should you get Uni Card?

As always, it relies on your profile and your requirements. To sum up, You get the following advantages with the Uni card:

- Lifetime Free Card

- Freebies: Mask+Chocolate+baggage tag

- Cashback: 1% cashback on all spending – applicable if your other cards don't give rewards/CB on certain txns

- Pay Later: It's like a 0% EMI card for three months – instrumental on high value/emergency spending.

- Offers: Zomato pro for three months – we may have more such requests in the future.

Except for the rewards, it scores well in most other aspects. If you're new to credit cards, it makes a lot of sense to hold one.

How to Apply?

Apply Via Android or IOS app

The application process is super simple. Just download the app and follow the process. It hardly takes ~5 minutes (or) less to complete.

They authenticate your identity via Aadhaar and a selfie.

The app uses CRIF to check eligibility. Still, once you proceed further and apply, it likely uses both CRIF & CIBIL reports together for under-writing, as I could see an inquiry on CIBIL via the NBFC partner (marked as NDXP, which is LiquiLoans).

Your virtual card will be instantly generated and ready for use as soon as you complete the application process. Just make sure you turn on "online transactions" via the app before going with your test charge.

The physical card reaches in approximately 3-5 days via Delhivery, and the good news is that you can choose your delivery address, just in case it's not the same as on Aadhaar – a pretty helpful feature.

Note: The card currently ships to select cities (~36 cities for now) and rapidly expands its footprint.

Final Thoughts

Overall the Uni Pay 1/3rd card has a good onboarding experience, premium welcome kit, reasonable credit limit, decent rewards, and a great support system. However, if you're into premium cards and just looking for "rewards," then this may not look attractive to you.

Uni Pay 1/3rd Card is certainly UNIque and overall gives an excellent experience for someone new to the world of credit cards.

That said, I would be highly interested in seeing a premium credit card from Uni Cards – perhaps a black card with black chocolate.

{kind=link}